John Hancock No Exam Life Insurance (Up To $3,000,000!)

John Hancock, a life insurance carrier with a long rich history, offers life insurance without a required medical exam – for those who qualify.

Don’t worry, we know another hassle is the last thing you need. Over the years, the application process has changed for the better, but varies according to the type and amount of coverage you want to buy.

– John Hancock

Here, you’ll find a comprehensive review of John Hancock’s no exam term life insurance products, called Protection Term.

Before applying for a policy, you’ll want to have a clear understanding of a particular carrier’s product and underwriting process. Why? No two no exam life insurance policies are the same.

Table Of Contents

John Hancock Life Insurance History

Founded in 1862, John Hancock Life Insurance Company has been in business for over 150 years.

They are headquartered in Boston, MA and conduct business throughout the United States.

Its name, John Hancock, was selected by the founders to represent integrity. Presently, the life insurance company is a division of a financial corporation based out of Toronto, Canada, called Manulife Financial.

To date, John Hancock has provided insurance products to more than 2.6 million policyholders (as of 2018).

Financial Strength Rating: A+ (A.M. Best)

Interesting fact – In 2015, John Hancock partnered with Vitality Group. They are the first insurance company in the United States to incentivize their clients to live healthy lives through “wellness-based rewards”.

John Hancock No Exam Life Insurance

Let’s take a quick glance at the main features of John Hancock’s no medical exam term life insurance, called Protection Term.

When deciding on the best life insurance policy to apply for, there are a number of top factors to consider:

- Wait time – How long it takes for my life insurance policy to be issued.

- Issue ages – The age range the carrier is willing to insure.

- Policy amount – The amount of life insurance you can buy.

- Term length – The length of time your policy can last.

- No exam – The specific underwriting process.

How Does John Hancock Measure Up?

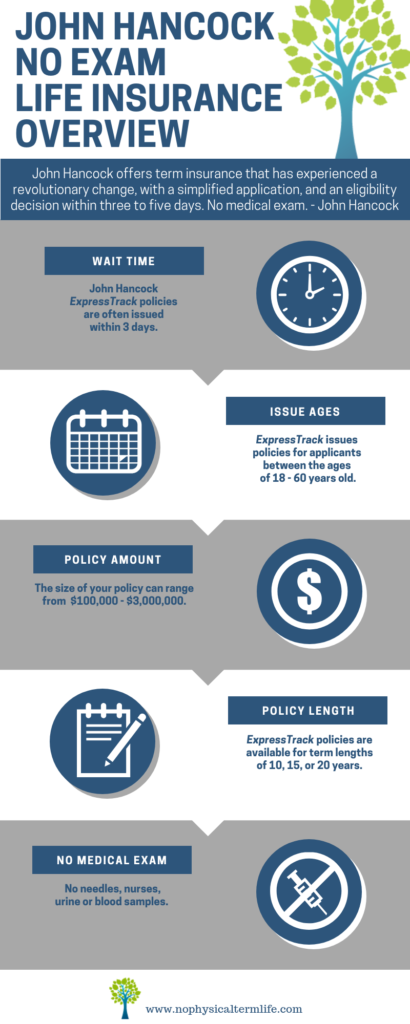

1. Wait Time

If you qualify for the ExpressTrack, your policy can be issued in as little as 3 – 5 days.

Called Accelerated Underwriting, based on your phone interview and application, it’s possible to bypass the needles and nurses.

John Hancock’s “no-touch” ExpressTrack program is available to generally healthy individuals who qualify for any health class from Standard to Super Preferred.

If you do not qualify for ExpressTrack, you will need to participate in medical underwriting.

Expect to wait approximately 30 days for your policy to be issued due to the processing of lab work and possible review of physician’s statements (APS).

2. Issue Ages

John Hancock issues no exam life insurance for applicants between the ages of 18 – 60.

If you are older than 60, consider evaluating your options for no exam life insurance for seniors.

Specific to term life insurance, the following carriers offer no exam policies to applicants older than 60:

- American National Life Insurance

- Phoenix Life Insurance

- Foresters Life Insurance

- Sagicor Life Insurance

- Fidelity Life Insurance

3. Policy Amount

John Hancock now issues no medical exam life insurance in face amounts from $100,000 – $3,000,000.

$3 million is an uncommon face amount for policies that skip medical underwriting.

4. Term Length

John Hancock offers no exam life insurance policies for 10, 15, and 20-year term lengths AND permanent single-life policies.

Note – It’s best to secure a policy that will last as long as your loved ones need financial protection. If the need is indefinite, evaluate your no exam whole life insurance options.

5. No Exam (if you qualify)

Based on your application and phone interview, you may be eligible to skip medical underwriting – needles, nurses, and liquid samples.

Keep in mind, though, with John Hancock’s accelerated underwriting, it’s not guaranteed that you will bypass the medical exam.

You may want to evaluate the top no physical life insurance companies as some carriers never require a medical exam during underwriting.

Riders

You will also want to be familiar with a product’s riders as they are often overlooked.

What are riders?

Riders are features (contractual provisions) to your life insurance policy, in addition to the death benefit.

Should you encounter a hardship, riders can make all the difference.

John Hancock offers one important rider for their ExpressTrack products.

Long-Term Care Rider

The Long-Term Care Rider (LTC) is available for purchase. Also referred to as an accelerated death benefit, this rider provides the option to accelerate a portion of your death benefit should you meet qualifying conditions.

John Hancock Application Process

Remember, John Hancock uses an accelerated underwriting process, called ExpressTrack.

Essentially, by participating in their application, it will be determined if you qualify to skip the medical exam.

ExpressTrack steps:

Step 1

We highly recommend you partner with an independent agent. This is optional, of course.

An independent agent will work on your behalf to obtain multiple quotes from multiple carriers. That way, you can be sure you are finding the best policy to fit your needs at the best rate you qualify for.

John Hancock’s life insurance policy might be your best option, or there may be another carrier who meets your specific needs.

Step 2

You will submit an electronic (or paper) ticket to John Hancock. The ticket initiates your application process.

You will automatically be considered for the ExpressTrack, no medical exam, process.

Step 3

A John Hancock representative will get in touch with you for a phone interview.

Plan to answer questions pertaining to:

- Birthday

- Gender

- Height/weight

- Occupation

- Medical history

- Prescription history

- Medical history of close blood-related relatives (siblings, parents)

- Tobacco use, alcohol or drug use

- Lifestyle

- Military status

- Beneficiaries

The phone interview typically lasts between 20 – 30 minutes.

Step 4

A John Hancock underwriter (their job is to assess risk) will review your application, interview, and records (driving, prescription, Medical Information Bureau) to determine whether or not you qualify for no exam life insurance.

Note – while not an exhaustive list, the following are common impairments and/or lifestyle factors that will disqualify you for ExpressTrack:

- Diabetes

- Cancer history (basal and squamous cell skin cancer is okay)

- Autoimmune disorders

- Alcoholism

- Fatty liver

- Hepatitis

- Hazardous sports (resort diving is okay)

- Professional athletes

- DUI (Driving Under the Influence conviction)

- Bankruptcy within the last 5 years

- Criminal history

- Prior applications within the last 12 months

Important – John Hancock will request a post-issue attending physician’s statement (APS) for every ExpressTrack policy.

Step 5

Decision time. You will receive one of two answers based on your application:

- ExpressTrack Qualifier – “No-touch” decision. You qualify for life insurance at a health class from Standard to Super Preferred.

- Traditional Underwriting – You require additional underwriting and will participate in a paramedical exam.

Important – Sometimes applicants are declined life insurance. Do not fret. There are always options, including guaranteed issue life insurance for those who would otherwise not qualify for coverage.

John Hancock Quotes

Let’s consider some sample rates. Quotes are for 10-year term policies.

John Hancock Quotes Male

| $100,000 | $500,000 | $1,000,000 | $3,000,000 | |

|---|---|---|---|---|

| 20 year old | $9.85 | $18.77 | $30.71 | $75.06 |

| 30 year old | $9.85 | $18.98 | $31.05 | $76.09 |

| 40 year old | $10.92 | $21.07 | $34.80 | $87.35 |

| 50 year old | $16.55 | $42.48 | $76.43 | $212.23 |

| 60 year old | $37.53 | $114.34 | $214.79 | $627.30 |

John Hancock Quotes Female

| $100,000 | $500,000 | $1,000,000 | $3,000,000 | |

|---|---|---|---|---|

| 20 year old | $8.91 | $14.50 | $22.86 | $51.52 |

| 30 year old | $8.91 | $15.10 | $23.03 | $52.03 |

| 40 year old | $9.64 | $20.47 | $29.86 | $72.51 |

| 50 year old | $15.44 | $35.31 | $62.27 | $169.75 |

| 60 year old | $29.00 | $77.54 | $141.60 | $407.73 |

John Hancock Vitality Program

John Hancock Vitality is an innovative program that rewards clients for healthy behaviors.

Save money and earn valuable rewards by simply living a healthy life.

– John Hancock Vitality Program

If you participate in the Vitality Program, you qualify for:

- Possibly saving money on your life insurance premiums

- Save on healthy food purchases at select grocery stores

- Opportunity to earn an Apple Watch Series 2 through workouts

- Rewards for entertainment, shopping, gym, and travel

Your Vitality Rewards may vary based on the type of insurance policy. Further, program benefits are only accessible to the insured person under the eligible life insurance policy.

Quit Smoking Incentive

John Hancock uses a unique program called, Quit Smoking Incentive (QSI). If you are a current smoker in need of life insurance, you may qualify for non-tobacco rates if you successfully participate in the program.

Quit Smoking Incentive details:

- Non-tobacco rates for the first 3 years

- Insured must sign a tobacco usage supplement

- Verifies no tobacco use of at least 12 months with a urinalysis sample

- Eligible for ages 20 – 70

- Not available for substandard health ratings

Important – QSI is only available for permanent life insurance products with a minimum of $50,000 face value.

Apply For Life Insurance

Whether a policy through John Hancock makes sense or another carrier, you will want to do two things:

- Collaborate with an independent agent. This can be done completely online or over the phone. They will access the top carriers to find the best policy at the best rate that you qualify for.

- Prepare. Have your important information readily available to communicate during the application process. We’re talking about your medical history, occupation, and lifestyle information.

To get started, simply fill out our free online quote.

8 Comments

ethel henderson

neen a quotes for me

ethel henderson

quotes on me

Heidi Mertlich

Hi Ethel, Thanks for getting in touch. The best way to start the quoting process is to fill out our free quote form.

Linda D Harkins

Looking for life insurance (whole) that won't go up, up, up.

Linda D Harkins

Do not know what ROI means.

Heidi Mertlich

Hi Linda, Thanks for reaching out. You have plenty of whole life insurance options in which your premiums remain level. You can fill out our free quote tool to view options. Simply select "Lifetime" under the "Type of Insurance" section.

ROI typically means "return on investment".

Shabreeka Dobbins

I’m needing help finding insurance I did quote I’m looking to get whole which if term the only option I’ll take please can you reach out

Bennett Bier

We tried reaching out but were not able to connect to go over the no exam life insurance options. Please call at your convenience 800-611-9622.